Hello everyone,

Last month, I commented that when December has been a challenging month in the stock market, investors may look to historical trends such as the January Effect to gauge potential performance in the upcoming month. The January Effect is a phenomenon where the stock market tends to experience positive returns in January following a weak December (www.themoneychimp.com/features/monthly_returns.htm).

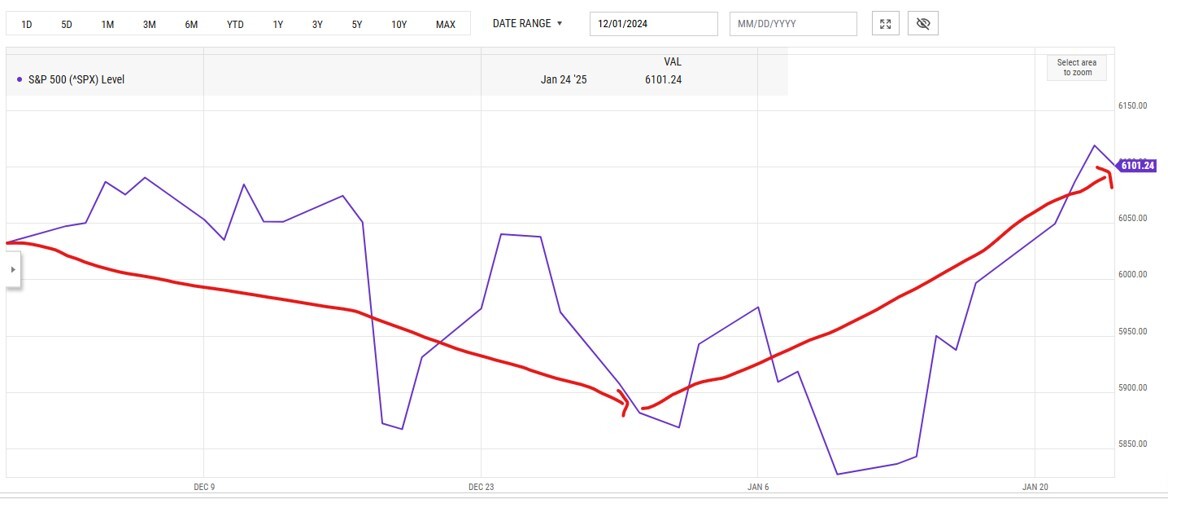

Well, looks like the January Effect came through. After a weak performance in December on the S&P500, posting a loss of -2.50%, the troops advanced the line and gained more ground adding a whopping 3.70% gain at the time of this writing. This gives us an overall performance of a net gain of 1.20% since December 1st of 2024.

The question on everyone's mind is: can it last? In my opinion, I believe so. However, it depends on several factors and the first being that for sustained growth, the US needs to avoid recession. Given the current status, I think we'll get a checkmark. Historical data suggests that in the third year of a bull market, average gains of approximately 5% can be achieved if economic downturn is prevented (https://biztechweekly.com/sp-500-rally-4-critical-factors-shaping-market-outlook-for-2025/). I had mentioned a few editorials ago, that a 10% growth target was assigned to the S&P500 for 2025 but we were already half way there in November of 2024 (https://advisors.td.com/rietzedukeassociateswealthmanagement/november24.htm?utm_source=GMB&utm_medium=link&utm_campaign=local&y_source=1_OTEyMDkwOC0

3MTUtbG9jYXRpb24ud2Vic2l0ZQ%3D%3D), which brings me to my second point. In order for this to happen, corporate earnings growth is crucial to sustain the upward movement in stock prices. Analysts agree that for this to fruition, we'll need a stable economy and further advancement in AI technology (https://biztechweekly.com/sp-500-rally-4-critical-factors-shaping-market-outlook-for-2025/). Another checkmark for this point. DeepSeek is paving the way to cheaper and groundbreaking development in AI.

Next, the Federal Reserve's monetary policies also hold weight in market performance. Despite recent signals leaning towards a more stringent approach, market expectations lean towards a more accommodative stance with potential interest rate cuts in 2025. Historically, the S&P 500 has fared well following periods of Fed rate reductions, especially when not accompanied by a recession.

Lastly, the policies implemented by the incoming Trump administration (2.0) could significantly influence the market's performance. Factors such as tariffs, tax reforms, and deregulation are expected to play key roles. While deregulation may benefit sectors like financial services and energy, tariffs pose possible risks. Tax reform may encounter legislative challenges and may not have a substantial impact until later in 2026. This could be a huge risk for the Republicans because they'll be up for re-election and voters may not see the benefits before then and thus have a change of heart.

I know there are doubters out there, and you'll have own thesis, which is fair. However, I am going to challenge that by historical statistics. Since 1928, the S&P500 (my apologies that I keep referring to the U.S., however, we are the 51st state now, lol), has repeatedly posted gains in the year that follows consecutive double digit return years. More notably in the 90's, from 1995 to 1999. Some great years. There's also 1950 to '51, 1954 to '55 and more recently 2019 and 2020 but I'm not sure we should include the COVID years, as that was an anomaly. With all that said, there has been years where the S&P500 corrected significantly, the largest decline in 1937 of -38.6%, with its runner up being 2022 of -19.4%. The moral of the story here is that for years that follow strong performance, it doesn't necessarily mean that the markets are due for a big correction, the odds are in our favour.

So, what can we figure for February? Albeit I've painted a picture of unicorns and rainbows, but February has historically been a tumultuous month for the stock market. Analysts and investors often brace themselves for potential volatility and downturns in stock prices during this time. Historical data has consistently shown that February ranks among the worst months for stock market performance. Argh!

Several factors contribute to the typically challenging environment for the stock market in February. One of the primary reasons is the phenomenon known as the "February effect," (lol, sound familiar?), where many investors tend to sell off stocks for tax-related purposes after the turn of the new year. I can attest to that! This can lead to increased selling pressure and market declines. Additionally, lower trading volumes and liquidity in February can exacerbate market movements, potentially leading to heightened volatility.

Another reason for the historically poor performance of the stock market in February is the seasonality effect. Some investors pay attention to historical patterns and tend to reduce their exposure to equities during this time, leading to weaker demand for stocks and potential downward pressure on prices.

It's important to note that while February has a track record of challenging stock market performance, this does not mean that every February will follow the same pattern. Market conditions and investor behavior can vary widely from year to year, making it essential for us to approach February with caution but also an understanding of the broader market dynamics at play.

As always, I'm around should you want to chat. And with that, I'll end it here, until next month!

The information contained herein has been provided by Rietze Duke & Associates Wealth Management and is for information purposes only. The information has been drawn from sources believed to be reliable. Graphs and charts are used for illustrative purposes only and do not reflect future values or future performance of any investment. The information does not provide financial, legal, tax or investment advice. Particular investment, tax, or trading strategies should be evaluated relative to each individual's objectives and risk tolerance.

Commissions, management fees and expenses all may be associated with investments in exchange-traded funds (ETFs). Please read the prospectus and ETF Facts before investing. ETFs are not guaranteed, their values change frequently and past performance may not be repeated. ETF units are bought and sold at market price on a stock exchange and brokerage commissions will reduce returns.

Certain statements in this document may contain forward-looking statements (“FLS”) that are predictive in nature and may include words such as “expects”, “anticipates”, “intends”, “believes”, “estimates” and similar forward-looking expressions or negative versions thereof. FLS are based on current expectations and projections about future general economic, political, and relevant market factors, such as interest and foreign exchange rates, equity and capital markets, the general business environment, assuming no changes to tax or other laws or government regulation or catastrophic events. Expectations and projections about future events are inherently subject to risks and uncertainties, which may be unforeseeable. Such expectations and projections may be incorrect in the future. FLS are not guarantees of future performance. Actual events could differ materially from those expressed or implied in any FLS. A number of important factors including those factors set out above can contribute to these digressions. You should avoid placing any reliance on FLS.

Source: London Stock Exchange Group plc and its group undertakings (collectively, the “LSE Group”). © LSE Group 2026. FTSE Russell is a trading name of certain of the LSE Group companies. “FTSE®”, “Russell®”, and “FTSE Russell®” are trademarks of the relevant LSE Group companies and are used by any other LSE Group company under license. “TMX®” is a trademark of TSX, Inc. and used by the LSE Group under license. All rights in the FTSE Russell indexes or data vest in the relevant LSE Group company which owns the index or the data. Neither LSE Group nor its licensors accept any liability for any errors or omissions in the indexes or data and no party may rely on any indexes or data contained in this communication. No further distribution of data from the LSE Group is permitted without the relevant LSE Group company’s express written consent. The LSE Group does not promote, sponsor or endorse the content of this communication. Index returns are shown for comparative purposes only.

Indexes are unmanaged and their returns include reinvestment of dividends, if applicable, but do not include any sales charges or fees as such costs would lower performance. It is not possible to invest directly in an index.

Links to other websites are for convenience only. No endorsement of any third-party products, services or information is expressed or implied by any information, material or content referred to or included on or linked from or to here.

TD Asset Management Inc. is a wholly-owned subsidiary of The Toronto-Dominion Bank.

Rietze Duke & Associates Wealth Management is part of TD Wealth Private Investment Advice, a division of TD Waterhouse Canada Inc. which is a subsidiary of The Toronto-Dominion Bank.

®The TD logo and other TD trademarks are the property of The Toronto-Dominion Bank or its subsidiaries.