Understanding what you pay is an important part of investing. Years ago, regulators required all investment firms to provide annual reports highlighting how much investors are paying their advisor, but what was missing was the individual product costs.

Total Cost Reporting (TCR) is a new regulatory requirement designed to enhance transparency of investment costs. Beginning in 2027, clients are to receive an annual, easy to read report disclosing all fees associated with mutual funds, ETFs, and other in-scope investments. It will provide investors with increased awareness of all fees and costs paid, in dollars and percentages. It is important to know, these are NOT new fees. It is a move to wholesome fee transparency to promote competition and help investors determine value for services paid.

What you need to know

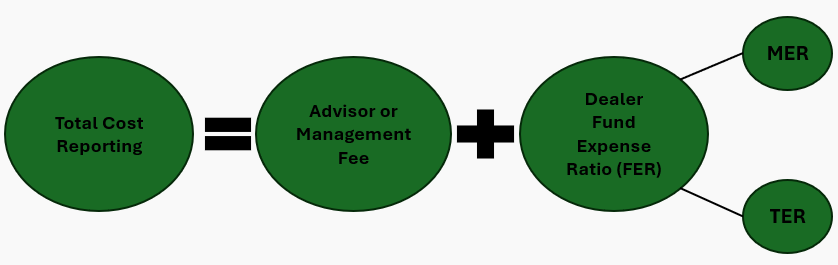

New reporting will show embedded Fund Expense Ratio (FER) for each holding. FER is made up of two components:

- Management Expense Ratio (MER) – The annualized percentage cost of management fees, operation expenses, custody, audit, legal, regulatory filings, and taxes.

- Trading Expense Ratio (TER) – A lesser-known expense for buying and selling securities within the fund. Only equity funds have TER's whereas bond funds do not.

Firms begin collecting the data January 1, 2026, and you will receive your first comprehensive report summarizing all of 2026 in January 2027.

Why this matters to investors

It is important to recognize that these are not new fees, rather, an improved and more in-depth reporting that makes all costs easier to review and compare. Seeing a single cost number for the first time can feel unsettling — it makes the invisible visible. We celebrate these changes and have been proactively having conversations with our clients.

Am I paying too much?

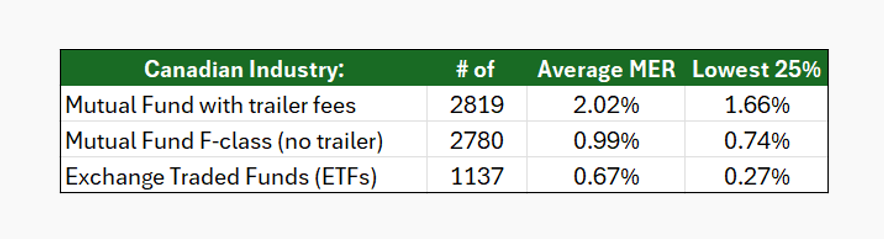

Below are Canadian industry average costs of key products, as well as the cheapest 25%. These figures only reflect MERs because TERs are not as easy to access and compile.

When paying more can be appropriate

When it comes to building your portfolio, it's easy to be drawn toward the lowest cost option. The cheapest isn’t always the best value nor may it help achieve your goals. True value lies in understanding what you're actually paying for. For certain parts of a portfolio, paying a premium can be justified if the investment fills a specific role:

- Investments that diversify and stabilize returns.

- Strategies that capture more upside return than downside.

- Unique strategies that cannot be replicated by a low-cost option.

Bottom line

Total Cost Reporting won’t tell you which investment is best, but it will give you a clear, comparable number when evaluating value for fees paid. We feel it is important to keep the focus on value and outcomes, not just price.

Our goal is to be viewed as a leader within the industry and help our clients and investors by providing complete transparency and total wealth management services, in the hopes to add value, deepen trust and meet their goals!

Until next time...

Invest Well. Live Well.

**The views expressed are those of Eric Davis, Senior Portfolio Manager and Senior Investment Advisor, Keith Davis, Associate Investment Advisor, and Heidi Bradley, Associate Investment Advisor, of TD Wealth Private Investment Advice, as of February 15, 2026, and are subject to change based on market and other conditions.**

Commissions, management fees and expenses all may be associated with mutual fund and/or exchange-traded fund ("ETF") investments (collectively, "the Funds"). Trailing commissions may be associated with mutual fund investments. ETF units are bought and sold at market price on a stock exchange and brokerage commissions will reduce returns. Please read the fund facts or summary documents and the prospectus, which contain detailed investment information, before investing in the Funds. The indicated rates of return (other than for money market funds) are the historical total returns for the period, compounded for mutual funds, including changes in unit value and reinvestment of distributions. The indicated rate of return for each money market fund is an annualized historical yield based on the seven-day period ended as indicated and annualized in the case of effective yield by compounding the seven day return and does not represent an actual one year return. Index returns do not represent ETF returns. The indicated rates of return do not take into account sales, redemption, commission charges, distribution or optional charges, as applicable, or income taxes payable by any securityholder that would have reduced returns. The Funds are not covered by the Canada Deposit Insurance Corporation or by any other government deposit insurer and are not guaranteed or insured. Their values change frequently. There can be no assurances that a money market fund will be able to maintain its net asset value per unit at a constant amount or that the full amount of your investment will be returned to you. Past performance may not be repeated.

®The TD logo and other TD trademarks are the property of The Toronto-Dominion Bank or its subsidiaries.